")

Buying your first home can feel overwhelming — especially when you start hearing terms like FHA, conventional 97, DPA, or USDA. The good news? There are legitimate, government-backed and lender-supported programs specifically designed to help first-time buyers get into a home sooner.

Here’s a clear, practical breakdown of the most important programs you should know about.

1. Federal Housing Administration (FHA Loans)

F1HA loans are one of the most popular options for first-time buyers — and for good reason.

Why buyers like FHA loans:

-

Down payment as low as 3.5%

-

More flexible credit score requirements

-

Higher debt-to-income ratio allowances

-

Competitive interest rates

What to know:

-

You’ll pay mortgage insurance premiums (MIP).

-

Property must meet FHA appraisal standards.

-

Not limited strictly to first-time buyers, but commonly used by them.

Source: U.S. Department of Housing and Urban Development (HUD)

2. Fannie Mae HomeReady® Program

This is a conventional loan program designed for low-to-moderate income borrowers.

Highlights:

-

Down payment as low as 3%

-

Reduced private mortgage insurance (PMI) costs

-

Can use income from household members (even if they’re not on the loan)

-

Homebuyer education required

Great option if your credit is solid but your savings are tight.

Source: Fannie Mae Selling Guide

3. Freddie Mac Home Possible®

Similar to HomeReady, this conventional loan program is designed to make homeownership accessible.

Key features:

-

3% down payment option

-

Flexible income sources

-

Reduced mortgage insurance options

-

Available for single-family homes and some multi-unit properties

Source: Freddie Mac Single-Family Guide

4. U.S. Department of Agriculture (USDA Loans)

If you’re buying in a qualified rural or suburban area, this program is powerful.

Why it’s attractive:

-

0% down payment

-

Competitive interest rates

-

Lower mortgage insurance costs than FHA

Important:

-

Property must be in an eligible area.

-

Income limits apply.

Many buyers are surprised to learn that many suburban areas qualify.

Source: USDA Rural Development

5. U.S. Department of Veterans Affairs (VA Loans)

For eligible veterans, active-duty service members, and certain military spouses.

Major advantages:

-

0% down payment

-

No private mortgage insurance

-

Competitive interest rates

-

Flexible credit requirements

This is widely considered one of the strongest loan programs available.

Source: VA Home Loan Program Guide

6. Down Payment Assistance (DPA) Programs

Beyond loan types, many buyers overlook local and state assistance programs.

These may include:

-

Grants (money you don’t repay)

-

Forgivable loans

-

Deferred second mortgages

-

Closing cost assistance

Programs vary by state and even by county. Many are funded through state housing finance agencies or local housing authorities.

To search:

-

Check your state’s housing finance agency website

-

Visit HUD’s local homeownership assistance page

-

Ask your lender about layered assistance programs

What Qualifies You as a “First-Time Buyer”?

According to HUD, you’re considered a first-time homebuyer if:

-

You haven’t owned a home in the last three years

-

You’re a single parent who previously owned with a spouse

-

You’re a displaced homemaker

-

You’ve only owned property not permanently affixed to a foundation

That definition surprises a lot of people.

A Practical Tip Before You Apply

Before choosing a program:

-

Review your credit score.

-

Calculate your debt-to-income ratio.

-

Estimate how much cash you can comfortably use for down payment + reserves.

-

Compare long-term cost (including mortgage insurance).

The “lowest down payment” option is not always the most cost-effective over time.

Final Thoughts

First-time homebuyer programs exist to reduce barriers — but they’re not one-size-fits-all. The right option depends on:

-

Your credit profile

-

Your income

-

Your long-term plans

-

The location of the home

If you’re early in the process, the smartest move is getting pre-approved and having a lender run multiple scenarios.

Homeownership is achievable — especially when you understand the tools available to you.

Disclaimer

The information provided in this article is for general educational and informational purposes only and should not be considered financial, legal, tax, or mortgage advice. Loan programs, eligibility requirements, income limits, credit score guidelines, interest rates, and down payment assistance availability may change without notice and can vary by lender, location, and individual borrower profile.

Program details referenced from sources such as the Federal Housing Administration (FHA), Fannie Mae, Freddie Mac, U.S. Department of Agriculture (USDA), U.S. Department of Veterans Affairs (VA), and the U.S. Department of Housing and Urban Development (HUD) are summarized for convenience and may not reflect the most current guidelines.

Readers should consult with a licensed mortgage lender, financial advisor, tax professional, or real estate professional to obtain advice tailored to their specific circumstances before making any home purchase or financing decisions. Nothing in this article constitutes a commitment to lend or guarantee loan approval.

Download these helpful checklists to guide you through your buying and selling journey.

")

Home Buyer’s Checklist

")

Home Seller’s Checklist

")

Mistakes To Avoid

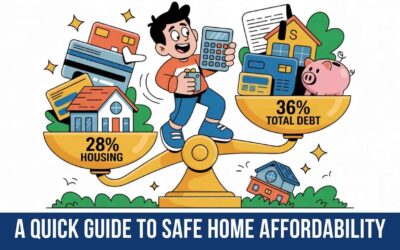

A Quick Guide to Safe Home Affordability: The 28/36 Rule Explained

Buying a home is exciting — but figuring out how much house you can safely afford can feel overwhelming. One of the simplest guidelines many lenders and financial advisors use is called the 28/36 Rule. It’s not a strict law, but it’s a widely accepted affordability...

Top 10 States With Affordable Housing in 2026

If you're house-hunting and trying to stretch your dollar further, location matters — a lot. Based on 2026 median home values, rent prices, cost of living data, and property tax rates, here are 10 states where affordability still exists. (Sources referenced include...

Should You Buy Now or Wait? A Practical (and Honest) Guide for Homebuyers

If you’re asking this question, you’re not alone. Almost every serious buyer eventually wonders: “Should I buy now… or should I wait for rates to drop and prices to cool?” Let’s break this down logically, using real data, economic fundamentals, and practical...

")

![]()

Commercial and Residential

Referral Division

Download Fair Housing Notice

Master Disclaimer

The views, opinions, and summary statements expressed in the contents of this website are those only of the noted presenter(s) (herein referenced as “opinion”) and do not represent official policy or policy positions of eXp World Holdings, it’s subsidiaries or vendor partners or clients (herein reference as “eXp”).

The contents of the media presented on this website and any media cross referenced as related to David G. Reis carry such disclaimers as above.

Quantitative information regarding real estate listings or industry statistics has been derived from source documents with appropriate permissions.

The accuracy of such information is the responsibility of the authors/owners of such source documents.

The media in this website makes no representation of the operational and business models,

expenses or financial success of licensed real estate professionals at, joining, or considering joining eXp.