Buying a home in North America often starts with one big financial hurdle: the down payment. While the traditional idea of saving 20% of a home’s price can feel overwhelming, the good news is that many buyers reach their goal faster with smart strategies and disciplined planning.

Here are practical, realistic ways to accelerate your down payment savings and move closer to owning your first home.

1. Set a Clear Target Amount

Start by determining exactly how much you need to save. In the U.S. and Canada, many loan programs allow down payments as low as 3%–5% for qualified buyers, though higher down payments can reduce monthly costs.

For example, if a $400,000 home requires a 5% down payment, your savings target would be $20,000, plus closing costs. Having a clear number helps you build a focused savings plan.

2. Automate Your Savings

One of the easiest ways to build savings quickly is automation. Set up automatic transfers from your checking account to a dedicated down payment savings account every payday.

Even modest contributions like $300–$500 per month add up significantly over time and remove the temptation to spend the money elsewhere.

3. Reduce Major Monthly Expenses

Small lifestyle adjustments can speed up savings. Consider:

-

Cutting unused subscriptions

-

Cooking at home more often

-

Downsizing temporary housing

-

Reducing discretionary spending

Saving $400–$700 per month from reduced expenses could add $5,000–$8,000 annually to your down payment fund.

4. Use Windfalls and Bonuses

Unexpected money can accelerate your progress dramatically. Consider directing these funds straight into your savings:

-

Tax refunds

-

Work bonuses

-

Side hustle income

-

Gifts from family

A $3,000 tax refund or year-end bonus can make a meaningful dent in your down payment goal.

5. Explore Down Payment Assistance Programs

Many first-time homebuyer programs in the U.S. and Canada offer grants or low-interest assistance for down payments and closing costs.

These programs may come from:

-

State or provincial housing agencies

-

Local governments

-

Employer housing benefits

Some buyers qualify for thousands of dollars in assistance, significantly reducing the savings required.

6. Open a Dedicated “House Fund”

Keeping your down payment savings separate from everyday spending money helps maintain discipline.

Many buyers use:

-

High-yield savings accounts

-

First-time homebuyer savings accounts

-

Dedicated investment or savings apps

Seeing your balance grow creates motivation and helps track progress.

7. Consider a Temporary Side Hustle

A short-term side hustle can dramatically accelerate savings. Examples include:

-

Freelance work

-

Tutoring or consulting

-

Selling unused items online

-

Weekend gig work

An extra $500–$1,000 per month could help you reach your goal months or even years sooner.

8. Track Your Progress and Stay Motivated

Set small goals, celebrate progress, and remember that every dollar saved moves you closer to owning your home.

Final Thoughts

Saving for a down payment may feel daunting at first, but with a structured plan and consistent habits, many buyers reach their goal faster than expected. By automating savings, cutting unnecessary expenses, and exploring assistance programs, you can turn homeownership from a distant dream into a realistic plan.

Disclaimer

This article is intended for general informational purposes only and should not be considered financial, mortgage, tax, or legal advice. Mortgage requirements, down payment programs, and affordability guidelines vary by lender, location, and individual financial circumstances. Homebuyers should consult with a licensed mortgage professional, financial advisor, or real estate professional to evaluate their specific situation before making financial decisions related to purchasing a home.

Download these helpful checklists to guide you through your buying and selling journey.

")

Home Buyer’s Checklist

")

Home Seller’s Checklist

")

Mistakes To Avoid

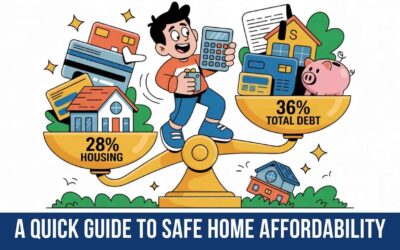

A Quick Guide to Safe Home Affordability: The 28/36 Rule Explained

Buying a home is exciting — but figuring out how much house you can safely afford can feel overwhelming. One of the simplest guidelines many lenders and financial advisors use is called the 28/36 Rule. It’s not a strict law, but it’s a widely accepted affordability...

Top 10 States With Affordable Housing in 2026

If you're house-hunting and trying to stretch your dollar further, location matters — a lot. Based on 2026 median home values, rent prices, cost of living data, and property tax rates, here are 10 states where affordability still exists. (Sources referenced include...

Should You Buy Now or Wait? A Practical (and Honest) Guide for Homebuyers

If you’re asking this question, you’re not alone. Almost every serious buyer eventually wonders: “Should I buy now… or should I wait for rates to drop and prices to cool?” Let’s break this down logically, using real data, economic fundamentals, and practical...

")

![]()

Commercial and Residential

Referral Division

Download Fair Housing Notice

Master Disclaimer

The views, opinions, and summary statements expressed in the contents of this website are those only of the noted presenter(s) (herein referenced as “opinion”) and do not represent official policy or policy positions of eXp World Holdings, it’s subsidiaries or vendor partners or clients (herein reference as “eXp”).

The contents of the media presented on this website and any media cross referenced as related to David G. Reis carry such disclaimers as above.

Quantitative information regarding real estate listings or industry statistics has been derived from source documents with appropriate permissions.

The accuracy of such information is the responsibility of the authors/owners of such source documents.

The media in this website makes no representation of the operational and business models,

expenses or financial success of licensed real estate professionals at, joining, or considering joining eXp.