Guide for Homebuyers (5)")

If you’re asking this question, you’re not alone. Almost every serious buyer eventually wonders:

“Should I buy now… or should I wait for rates to drop and prices to cool?”

Let’s break this down logically, using real data, economic fundamentals, and practical decision-making — without hype.

1. The Interest Rate Question

Mortgage rates fluctuate based on inflation, Federal Reserve policy, and bond market activity. According to the Federal Reserve, rate decisions are primarily driven by inflation control, not housing affordability.

When inflation rises:

-

The Fed tightens monetary policy.

-

Mortgage rates typically increase.

-

Borrowing becomes more expensive.

When inflation cools:

-

Rates may stabilize or decline.

-

Buying power improves.

However, here’s the key:

If rates drop significantly, demand usually increases — and home prices may rise due to competition.

This pattern has been observed repeatedly in housing cycles, including the post-2020 market surge reported by the National Association of Realtors.

So waiting for lower rates can sometimes mean:

-

Paying less interest

-

But paying more for the house itself

2. The Home Price Reality

According to long-term data from the U.S. Census Bureau and Federal Housing Finance Agency:

-

Home values historically trend upward over time.

-

Short-term corrections happen.

-

Long-term appreciation has averaged roughly 3–5% annually nationwide (varies by market).

This means timing the market perfectly is extremely difficult — even for economists.

3. The “Wait” Argument — When It Makes Sense

Waiting can be smart if:

-

Your credit score needs improvement

-

You have high-interest debt to pay down

-

You don’t have a stable emergency fund

-

Your job situation is uncertain

-

You plan to move again within 1–2 years

Buying too early can create financial strain. A house should build stability, not stress.

4. The “Buy Now” Argument — When It Makes Sense

Buying now may be logical if:

-

You plan to stay 5+ years

-

You have stable income

-

You have sufficient savings beyond your down payment

-

You’re comfortable with current monthly payments

-

Rent in your area is high and rising

Remember: you can refinance if rates fall. You cannot refinance the purchase price.

5. The Math Most Buyers Miss

Here’s what many overlook:

If prices rise 4% while you wait one year, but rates drop 0.5%…

You may still pay more overall due to:

-

Higher purchase price

-

Increased competition

-

Reduced negotiating power

Housing markets are driven by supply and demand — not just rates.

6. A Better Question to Ask

Instead of asking:

“Is this the perfect time to buy?”

Ask:

“Am I personally financially ready?”

The right time is less about national headlines and more about:

-

Your debt-to-income ratio

-

Your job security

-

Your savings cushion

-

Your long-term plans

Real estate is a long-term asset class — not a short-term trade.

Final Thought (Friendly Reality Check)

Trying to “time the market” perfectly is like trying to predict the exact day gas prices will be lowest before a road trip.

Possible? Maybe.

Reliable? Not really.

A well-prepared buyer in a stable financial position usually wins in the long run — regardless of minor market shifts.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial, legal, mortgage, or investment advice. Housing markets vary by location and individual financial circumstances. Please consult with a licensed mortgage professional, financial advisor, or real estate professional before making any home purchasing decisions. Past performance of real estate markets does not guarantee future results.

Download these helpful checklists to guide you through your buying and selling journey.

")

Home Buyer’s Checklist

")

Home Seller’s Checklist

")

Mistakes To Avoid

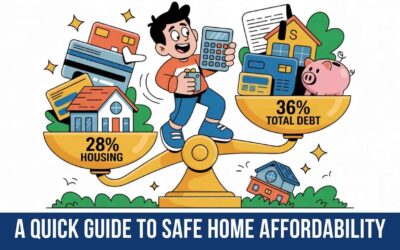

A Quick Guide to Safe Home Affordability: The 28/36 Rule Explained

Buying a home is exciting — but figuring out how much house you can safely afford can feel overwhelming. One of the simplest guidelines many lenders and financial advisors use is called the 28/36 Rule. It’s not a strict law, but it’s a widely accepted affordability...

Top 10 States With Affordable Housing in 2026

If you're house-hunting and trying to stretch your dollar further, location matters — a lot. Based on 2026 median home values, rent prices, cost of living data, and property tax rates, here are 10 states where affordability still exists. (Sources referenced include...

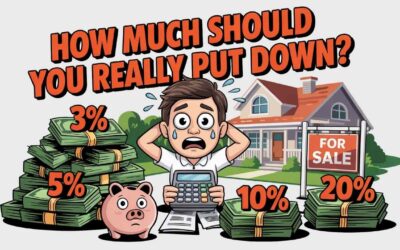

Down Payment Options: 3%, 5%, 10%, or 20%: What’s Best for You?

One of the biggest myths in real estate?“You need 20% down to buy a home.” That’s not always true. While a 20% down payment has advantages, many buyers — especially first-time homebuyers — purchase homes with far less. According to the National Association of Realtors...

")

![]()

Commercial and Residential

Referral Division

Download Fair Housing Notice

Master Disclaimer

The views, opinions, and summary statements expressed in the contents of this website are those only of the noted presenter(s) (herein referenced as “opinion”) and do not represent official policy or policy positions of eXp World Holdings, it’s subsidiaries or vendor partners or clients (herein reference as “eXp”).

The contents of the media presented on this website and any media cross referenced as related to David G. Reis carry such disclaimers as above.

Quantitative information regarding real estate listings or industry statistics has been derived from source documents with appropriate permissions.

The accuracy of such information is the responsibility of the authors/owners of such source documents.

The media in this website makes no representation of the operational and business models,

expenses or financial success of licensed real estate professionals at, joining, or considering joining eXp.